Cintas (CTAS US / Market cap $78bn) has agreed to acquire UniFirst (UNF US / Market cap $4.6bn) for an implied enterprise value of c. $5.5bn. UniFirst shareholders will receive $155.00 in cash and 0.7720 shares of Cintas stock for each UniFirst share held, representing $310.00 per share based on Cintas’ closing share price on 9th March 2026 (20.2% premium to 10th March close; 82% to the unaffected price immediately prior to announcement of a proposal on 22nd December).

The transaction has been unanimously approved by both boards, with closing subject to customary conditions including UniFirst shareholder approval and the receipt of required regulatory clearances. This should include HSR approval, while Canada is also likely to review, given both companies’ operations there. The DMA mentions reasonable best efforts covenants, but the companies aren't forced to agree to any structural or behavioural remedies. Cintas is subject to a $350m reverse termination fee.

Entities affiliated with the Croatti family, which control approximately two-thirds of UniFirst’s voting power across Common and Class B stock, have entered into a voting support agreement in favour of the transaction, materially increasing deal certainty. The transaction is expected to close in the second half of calendar 2026.

UniFirst has a dual-class share structure comprising Class A and Class B common stock. Class A shares, which are publicly traded, carry one vote per share, while Class B shares carry an enhanced ten votes per share and are primarily held by the Croatti family, giving them approximately two-thirds of the company’s voting power. As a result, the support of the Class B holders is effectively determinative for shareholder approval of the Cintas transaction.

This announced transaction follows a prolonged process dating back to 2022, rather than a new approach. Cintas first approached UniFirst in February 2022 with a $255 per share indication of interest, which was rejected. Cintas has since made unsuccessful unsolicited proposals for UniFirst, most recently a $275 per share cash proposal in December 2025, with limited engagement between the parties and proposals described as highly conditional. The current deal reflects a negotiated outcome supported by UniFirst’s board and controlling shareholders. Governance had long been a central factor given UniFirst’s Class B share structure and concentrated voting control, which meant that any transaction was unlikely to succeed without board endorsement and family support. With those elements now secured, the process shifts from approach and defence to regulatory review and shareholder approval.

Strategically, UniFirst would fold into Cintas’ core route-based offering. There is direct synergy between Cintas’ Uniform Rental and Facility Services segment, and the first aid activity would naturally sit alongside Cintas’ First Aid and Safety Services. The strategic logic is therefore simple, but it also makes the regulatory case harder as this is primarily a horizontal combination of two scaled providers in a route-based market where density and local footprint matter a lot when determining the level of competition.

The antitrust and regulatory review process, given significant operational overlap between the parties, could increase the likelihood of a second request. Both companies’ core businesses are uniform rental and bundled facility services delivered through local plants, branches and route-based service networks, creating potential competition issues in overlapping local service territories. On the deal call, Cintas' CEO was confident that no divestitures would be required.

Overview

UniFirst is a uniform rental and workplace services company. It picks up, washes and redelivers uniforms and workwear, usually on a weekly cycle, and also sells related items such as mats, wipes, restroom supplies and first aid products. Its customer base is broad, spanning manufacturing, retail and services. The business remains heavily weighted to its core uniform and facility operations, which accounted for about 91% of FY25 revenue, with first aid and safety at about 5% and the balance in other activities. The US is the main market, with Canada and Europe contributing a smaller share.

Cintas is the larger peer and the clear scale operator in the same market. Its core business is also uniform rental and facility services, but with broader adjacencies including first aid, safety, fire protection and direct sales. In fiscal 2025, Cintas generated about $10.3bn of revenue, of which roughly 77% came from uniform rental and facility services, 12% from first aid and safety, 8% from fire protection and 3% from direct sales. More than 90% of revenue comes from the US. The big difference versus UniFirst is scale: Cintas has a much broader network, with hundreds of facilities and thousands of routes.

Precedent Deals

The closest direct precedent is Cintas / G&K Services, announced in August 2016 and closed in March 2017. The deal took 217 days to close due to the FTC issuing a second request - approval took almost 7 months. Competition Canada also issued a supplementary information request, and took a similarly long time to clear the deal. The review process was lengthy and ultimately got cleared also thanks to the relatively fragmented market, and the presence of large competitors (Unifirst and Aramark (ARMK US / $10.5bn for instance) - now that G&K is part of Cintas, and the latter is going for Unifirst, the question is whether the market at the top can still be considered fragmented enough.

In the past, the DOJ has shown that in route-based service industries local depots, routes and density matter more than the headline national share. In the Advanced Disposal Services/Waste Management (WM US / $95bn) precedent, the DOJ said the deal would lessen competition in more than 50 local markets and required a large structural package, including landfills, transfer stations, hauling locations and collection routes. That is not the same industry, but the antitrust logic applies to different sectors alike - where the service is executed locally, and route density drives economics, regulators tend to focus on local market structure and fix problems with asset divestitures.

Stericycle/Healthcare Waste Solutions in 2011 points in the same direction. DOJ said the deal would reduce the number of competitors with local transfer stations in the New York metropolitan area from three to two and required the divestiture of the Bronx transfer station. Stericycle/MedServe in 2009 followed a similar pattern, with DOJ requiring the divestiture of treatment and transfer assets in Kansas, Missouri, Nebraska and Oklahoma after concluding the parties were the only two firms able to compete for larger customers in those areas. Again, the product is different, but the rationale is similar.

Taken together, these precedents show that regulators are comfortable using narrow local market definitions in route-based service industries. That does not mean Cintas/UniFirst is unfixable, but it makes a strong case for a lengthy review centred on local overlaps and possible asset remedies rather than a quick sail through approvals.

Overlap and Competitive Landscape

The transaction has been unanimously approved by both boards, with closing subject to customary conditions including UniFirst shareholder approval and the receipt of required regulatory clearances. This should include HSR approval, while Canada is also likely to review, given both companies’ operations there. The DMA mentions reasonable best efforts covenants, but the companies aren't forced to agree to any structural or behavioural remedies. Cintas is subject to a $350m reverse termination fee.

Entities affiliated with the Croatti family, which control approximately two-thirds of UniFirst’s voting power across Common and Class B stock, have entered into a voting support agreement in favour of the transaction, materially increasing deal certainty. The transaction is expected to close in the second half of calendar 2026.

UniFirst has a dual-class share structure comprising Class A and Class B common stock. Class A shares, which are publicly traded, carry one vote per share, while Class B shares carry an enhanced ten votes per share and are primarily held by the Croatti family, giving them approximately two-thirds of the company’s voting power. As a result, the support of the Class B holders is effectively determinative for shareholder approval of the Cintas transaction.

This announced transaction follows a prolonged process dating back to 2022, rather than a new approach. Cintas first approached UniFirst in February 2022 with a $255 per share indication of interest, which was rejected. Cintas has since made unsuccessful unsolicited proposals for UniFirst, most recently a $275 per share cash proposal in December 2025, with limited engagement between the parties and proposals described as highly conditional. The current deal reflects a negotiated outcome supported by UniFirst’s board and controlling shareholders. Governance had long been a central factor given UniFirst’s Class B share structure and concentrated voting control, which meant that any transaction was unlikely to succeed without board endorsement and family support. With those elements now secured, the process shifts from approach and defence to regulatory review and shareholder approval.

Strategically, UniFirst would fold into Cintas’ core route-based offering. There is direct synergy between Cintas’ Uniform Rental and Facility Services segment, and the first aid activity would naturally sit alongside Cintas’ First Aid and Safety Services. The strategic logic is therefore simple, but it also makes the regulatory case harder as this is primarily a horizontal combination of two scaled providers in a route-based market where density and local footprint matter a lot when determining the level of competition.

The antitrust and regulatory review process, given significant operational overlap between the parties, could increase the likelihood of a second request. Both companies’ core businesses are uniform rental and bundled facility services delivered through local plants, branches and route-based service networks, creating potential competition issues in overlapping local service territories. On the deal call, Cintas' CEO was confident that no divestitures would be required.

Overview

UniFirst is a uniform rental and workplace services company. It picks up, washes and redelivers uniforms and workwear, usually on a weekly cycle, and also sells related items such as mats, wipes, restroom supplies and first aid products. Its customer base is broad, spanning manufacturing, retail and services. The business remains heavily weighted to its core uniform and facility operations, which accounted for about 91% of FY25 revenue, with first aid and safety at about 5% and the balance in other activities. The US is the main market, with Canada and Europe contributing a smaller share.

Cintas is the larger peer and the clear scale operator in the same market. Its core business is also uniform rental and facility services, but with broader adjacencies including first aid, safety, fire protection and direct sales. In fiscal 2025, Cintas generated about $10.3bn of revenue, of which roughly 77% came from uniform rental and facility services, 12% from first aid and safety, 8% from fire protection and 3% from direct sales. More than 90% of revenue comes from the US. The big difference versus UniFirst is scale: Cintas has a much broader network, with hundreds of facilities and thousands of routes.

Precedent Deals

The closest direct precedent is Cintas / G&K Services, announced in August 2016 and closed in March 2017. The deal took 217 days to close due to the FTC issuing a second request - approval took almost 7 months. Competition Canada also issued a supplementary information request, and took a similarly long time to clear the deal. The review process was lengthy and ultimately got cleared also thanks to the relatively fragmented market, and the presence of large competitors (Unifirst and Aramark (ARMK US / $10.5bn for instance) - now that G&K is part of Cintas, and the latter is going for Unifirst, the question is whether the market at the top can still be considered fragmented enough.

In the past, the DOJ has shown that in route-based service industries local depots, routes and density matter more than the headline national share. In the Advanced Disposal Services/Waste Management (WM US / $95bn) precedent, the DOJ said the deal would lessen competition in more than 50 local markets and required a large structural package, including landfills, transfer stations, hauling locations and collection routes. That is not the same industry, but the antitrust logic applies to different sectors alike - where the service is executed locally, and route density drives economics, regulators tend to focus on local market structure and fix problems with asset divestitures.

Stericycle/Healthcare Waste Solutions in 2011 points in the same direction. DOJ said the deal would reduce the number of competitors with local transfer stations in the New York metropolitan area from three to two and required the divestiture of the Bronx transfer station. Stericycle/MedServe in 2009 followed a similar pattern, with DOJ requiring the divestiture of treatment and transfer assets in Kansas, Missouri, Nebraska and Oklahoma after concluding the parties were the only two firms able to compete for larger customers in those areas. Again, the product is different, but the rationale is similar.

Taken together, these precedents show that regulators are comfortable using narrow local market definitions in route-based service industries. That does not mean Cintas/UniFirst is unfixable, but it makes a strong case for a lengthy review centred on local overlaps and possible asset remedies rather than a quick sail through approvals.

Overlap and Competitive Landscape

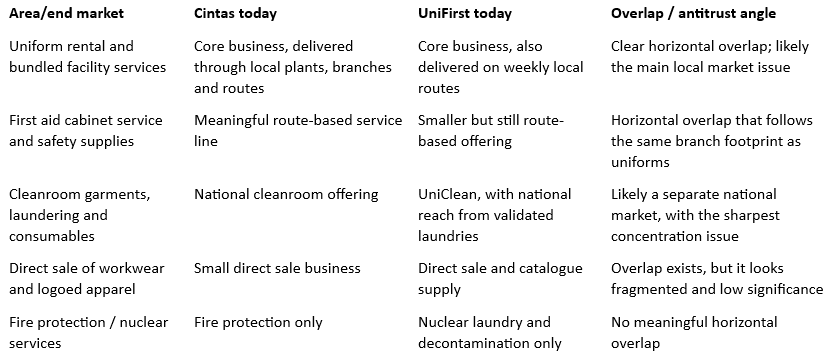

Fig 1: Overlap Analysis (Source: MKI)

This is mainly a horizontal deal, not a vertical or portfolio one. Both parties compete at the same stage of the chain, sell directly to end customers, and do not appear to have any supplier-customer relationship with each other. The real debate is therefore not foreclosure or data access. It is whether agencies define the relevant markets narrowly enough for the local route overlaps and cleanroom concentration to become difficult.

The competitive set looks broad at first glance, but tighter once the market is narrowed properly. UniFirst names Cintas, Alsco and Vestis (VSTS US / $1bn) as principal rental competitors, while Cintas describes its markets as local and highly fragmented. The combination could be viewed as #1 buying a fellow top 4 player in uniform and facility supplies, with pro forma share above 40%. Local uniform shares and national cleanroom shares are also cause for caution on a pro forma basis. On initial estimates, each of these markets exhibit combined profiles to indicate this is more than a marginal tuck-in. There are local markets within both parties' domain that might carry significant overlap and decrease the number of full-service providers. We will carry out more in-depth analysis in the coming days to determine a more precise footprint of states worth investigating further.

The broad textile rental market remains relatively fragmented, which is likely to form part of the parties’ competitive defence. However, the narrower uniform rental segment appears more concentrated, particularly at the local route level where large operators often dominate customer contracts, which may present a more challenging lens for antitrust review. The broad textile rental market remains relatively fragmented, which is likely to form part of the parties’ competitive defence. However, the narrower uniform rental segment appears more concentrated, particularly at the local route level where large operators often dominate customer contracts, which may present a more challenging lens for antitrust review. Market definition may also hinge on the distinction between rental and direct purchase of uniforms. Both companies offer customers rental and purchase options, and their filings note that buyers can switch between the two models; if regulators treat purchase as a credible substitute, the relevant market could broaden beyond rental-only services, reducing the apparent concentration in the core rental segment.

Likely Review Path and Key Regulatory Concerns

United States: Based on the precedents highlighted above, the FTC is likely to review this merger. The likely theories of harm are classic horizontal ones: loss of head-to-head competition in local uniform and facility-service routes, the same issue in first-aid cabinet servicing, and a separate national concentration problem in cleanroom. There's also a risk of a co-ordination angle in cities where the market could move closer to a two-player structure, mainly Cintas and Vestis. On precedent, a second request looks more likely than merely possible. G&K already drew one, and the current overlap set appears at least as sensitive in certain pockets. The more realistic debate is over remedy scope and timing, not whether agencies will take a hard look. The remedy template is likely to be structural - divestitures of local branches, routes and customer books in the tightest metros, with cleanroom the obvious area where a more material asset could be demanded.

On the deal call, as a first take, Cintas' CEO referenced that the company does not anticipate any divestitures, nor thinks there is any need for them.

State AGs: While there aren't many similar precedents where state AGs got involved, at first glanced we noticed a degree of overlap in California, Illinois, and Washington. Massachusetts and New York are also worth watching because they could take an interest if the review becomes contentious. The states would usually run in parallel with federal regulators, and would focus on local customer harm, branch density, and other overlaps.

Other Jurisdictions: Canada is worth watching because Cintas says its foreign operations are primarily there, and the earlier Cintas / G&K deal drew a supplementary information request from Competition Canada, but UniFirst’s non-US business is much smaller, with Europe and Canada together contributing only about $186m of FY25 revenue and no individual country accounting for more than 10 % of group revenue. That makes Canada a possible parallel workstream, but less likely to mirror the old G&K review in scale or importance, because this case is much more US-centred on the facts in hand.

Europe and the UK don't look concerning as Cintas’ non-US footprint is mainly Canada, while UniFirst’s European presence is small and appears concentrated in specialist operations, so neither the EC nor the CMA looks likely to be a core source of competition risk on the present record.

Conclusion

The strategic logic is simple, and so is the regulatory narrative. This is a horizontal combination in route-based uniform rental and facility services, where density and local footprint shape competition, and where the buyer is already the scale leader.

The core investor question is therefore whether the review becomes a debate about the probability of challenge, or a negotiation around remedy size and timing. The precedent pattern in concentrated route-based services suggests regulators will look closely at local overlaps and national account bidding dynamics, and will be most comfortable with structural divestitures where competition is tight, however initial commentary suggests no divestitures are anticipated. Cleanroom services, while smaller, could create an outsized remedy requirement if regulators see few credible alternatives in certain regions.

On process, the most realistic risk is an extended review with meaningful remedy discussions, rather than an immediate prohibition. That still matters for timing: even a “solvable” case can become a long one if the parties resist divestitures, or if governance constraints slow the path to a signed agreement in the first place.

Contact

Melanie Budden

melanie.budden@therealizationgroup.com

The competitive set looks broad at first glance, but tighter once the market is narrowed properly. UniFirst names Cintas, Alsco and Vestis (VSTS US / $1bn) as principal rental competitors, while Cintas describes its markets as local and highly fragmented. The combination could be viewed as #1 buying a fellow top 4 player in uniform and facility supplies, with pro forma share above 40%. Local uniform shares and national cleanroom shares are also cause for caution on a pro forma basis. On initial estimates, each of these markets exhibit combined profiles to indicate this is more than a marginal tuck-in. There are local markets within both parties' domain that might carry significant overlap and decrease the number of full-service providers. We will carry out more in-depth analysis in the coming days to determine a more precise footprint of states worth investigating further.

The broad textile rental market remains relatively fragmented, which is likely to form part of the parties’ competitive defence. However, the narrower uniform rental segment appears more concentrated, particularly at the local route level where large operators often dominate customer contracts, which may present a more challenging lens for antitrust review. The broad textile rental market remains relatively fragmented, which is likely to form part of the parties’ competitive defence. However, the narrower uniform rental segment appears more concentrated, particularly at the local route level where large operators often dominate customer contracts, which may present a more challenging lens for antitrust review. Market definition may also hinge on the distinction between rental and direct purchase of uniforms. Both companies offer customers rental and purchase options, and their filings note that buyers can switch between the two models; if regulators treat purchase as a credible substitute, the relevant market could broaden beyond rental-only services, reducing the apparent concentration in the core rental segment.

Likely Review Path and Key Regulatory Concerns

United States: Based on the precedents highlighted above, the FTC is likely to review this merger. The likely theories of harm are classic horizontal ones: loss of head-to-head competition in local uniform and facility-service routes, the same issue in first-aid cabinet servicing, and a separate national concentration problem in cleanroom. There's also a risk of a co-ordination angle in cities where the market could move closer to a two-player structure, mainly Cintas and Vestis. On precedent, a second request looks more likely than merely possible. G&K already drew one, and the current overlap set appears at least as sensitive in certain pockets. The more realistic debate is over remedy scope and timing, not whether agencies will take a hard look. The remedy template is likely to be structural - divestitures of local branches, routes and customer books in the tightest metros, with cleanroom the obvious area where a more material asset could be demanded.

On the deal call, as a first take, Cintas' CEO referenced that the company does not anticipate any divestitures, nor thinks there is any need for them.

State AGs: While there aren't many similar precedents where state AGs got involved, at first glanced we noticed a degree of overlap in California, Illinois, and Washington. Massachusetts and New York are also worth watching because they could take an interest if the review becomes contentious. The states would usually run in parallel with federal regulators, and would focus on local customer harm, branch density, and other overlaps.

Other Jurisdictions: Canada is worth watching because Cintas says its foreign operations are primarily there, and the earlier Cintas / G&K deal drew a supplementary information request from Competition Canada, but UniFirst’s non-US business is much smaller, with Europe and Canada together contributing only about $186m of FY25 revenue and no individual country accounting for more than 10 % of group revenue. That makes Canada a possible parallel workstream, but less likely to mirror the old G&K review in scale or importance, because this case is much more US-centred on the facts in hand.

Europe and the UK don't look concerning as Cintas’ non-US footprint is mainly Canada, while UniFirst’s European presence is small and appears concentrated in specialist operations, so neither the EC nor the CMA looks likely to be a core source of competition risk on the present record.

Conclusion

The strategic logic is simple, and so is the regulatory narrative. This is a horizontal combination in route-based uniform rental and facility services, where density and local footprint shape competition, and where the buyer is already the scale leader.

The core investor question is therefore whether the review becomes a debate about the probability of challenge, or a negotiation around remedy size and timing. The precedent pattern in concentrated route-based services suggests regulators will look closely at local overlaps and national account bidding dynamics, and will be most comfortable with structural divestitures where competition is tight, however initial commentary suggests no divestitures are anticipated. Cleanroom services, while smaller, could create an outsized remedy requirement if regulators see few credible alternatives in certain regions.

On process, the most realistic risk is an extended review with meaningful remedy discussions, rather than an immediate prohibition. That still matters for timing: even a “solvable” case can become a long one if the parties resist divestitures, or if governance constraints slow the path to a signed agreement in the first place.

Contact

Melanie Budden

melanie.budden@therealizationgroup.com