The transaction would require approval from both NextEra and Dominion shareholders, HSR antitrust clearance, FERC approval under Section 203 of the Federal Power Act, and NRC approval for the transfer of nuclear licences. The companies would also need state-level approvals from the Virginia SCC, the North Carolina Utilities Commission and the Public Service Commission of South Carolina.

Call at 9am ET: https://events.q4inc.com/attendee/660359299

A deal of this scale would unite the world's largest electric utility by market capitalization with the most strategically complex regulated utility franchise in the eastern United States, creating an entity operating across Florida, Virginia, South Carolina, North Carolina, and a vast unregulated renewables and generation platform spanning virtually every US power market. This note evaluates the full regulatory critical path, assigns probability-weighted timelines to each required approval, examines the precedent transaction record for both parties, contextualizes the current federal policy environment under the Trump administration, and provides a granular assessment of the Virginia State Corporation Commission (SCC), the single most consequential and uncertain regulatory forum for this deal.

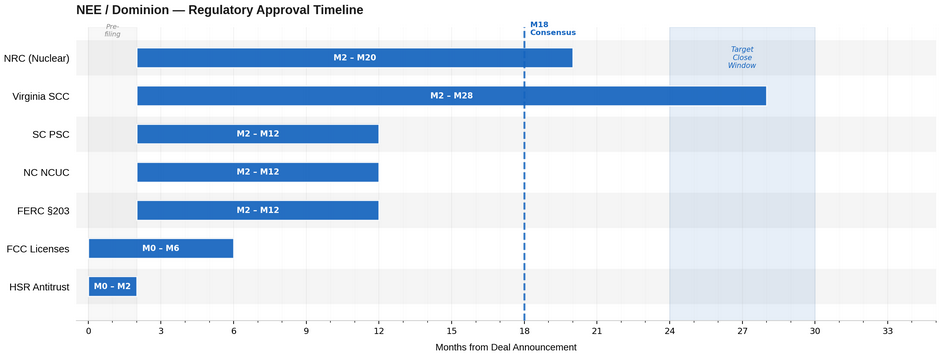

The central conclusion is that the Virginia SCC is not simply the hardest approval in the stack, it is a structurally unique proceeding, rendered even more complex by the current composition of the commission itself. Investors should treat Virginia as a binary risk item that cannot be adequately hedged through deal structure or pre-negotiated commitments alone. The realistic critical path, assuming parallel filings and no first-instance rejection, is 20-24 months from announcement to close, materially longer than the 12-18-month consensus framing and longer than either party's comparable precedent transactions. The Nuclear Regulatory Commission (NRC) is the second pacing item. All other approvals are surmountable on a normal litigation track.

It is worth noting the carry profile across an extended approval timeline. A long Dominion / short NextEra position would currently generate approximately 2% annual positive dividend carry, reflecting Dominion’s higher dividend yield (~4.5%) relative to NextEra (~2.5%), which may provide some support for utility / yield positioning even while the transaction remains pending.

The deal is not impossible, the investment logic is strong, NextEra's capital cost advantage is genuine, and the structural alignment between NEER's renewables capabilities and Dominion's VCEA obligations is substantive rather than cosmetic. But the regulatory critical path is longer, more uncertain, and more structurally novel - particularly at the Virginia SCC - than a headline market cap comparison would suggest. Investors should underwrite this as a 20-24-month regulatory process with a non-trivial risk of Virginia denial, not as a 12-18-month rate-of-return trade. The Deal Structure and Strategic LogicThe strategic logic here is clear. NextEra has for years strained against the ceiling imposed by its Florida concentration. Florida Power and Light serves over six million accounts in a single state; the regulated earnings base is deep but geographically inelastic. NextEra Energy Resources (NEER), by contrast, is the world's largest wind and solar developer and operator with approximately 37 GW of operating capacity, but it operates in competitive wholesale markets that are valued by public investors at a persistent discount to regulated utility earnings multiples. Acquiring Dominion Energy Virginia, a 2.8 million customer franchise in one of the fastest-growing load regions in the country, anchored by a massive data center build-out driven by Northern Virginia hyperscale demand, would add the most valuable regulated growth utility in North America to a balance sheet already optimized for large-scale capital deployment.

Dominion, for its part, faces a capital stack problem that the market has not rewarded. The Coastal Virginia Offshore Wind (CVOW) project, at 2.6 GW, achieved first power delivery to the PJM grid in March 2026 and is over 70% complete, representing an updated $11.5 billion in projected offshore construction expenditure. The Virginia Clean Economy Act (VCEA) obliges Dominion Energy Virginia to pursue a 100% carbon-free generation portfolio by 2045, with interim mandates for solar, onshore wind, and storage that require sustained capital outlays through the 2030s. Dominion's current balance sheet and credit profile price this program as a risk, while NextEra's capital cost and scale advantages price it as an opportunity. On that framing, the deal closes a genuine valuation gap rather than simply paying a control premium into a stagnant earnings stream.

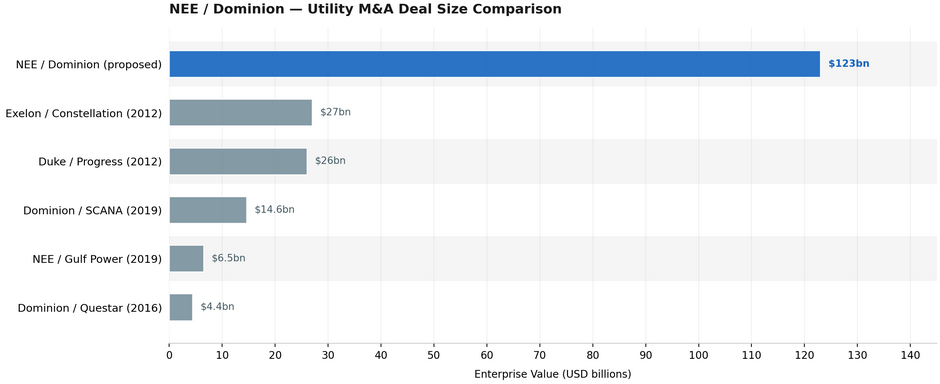

The total deal size, including Dominion's considerable debt load, would approach $120B billion in enterprise value, making it the largest utility acquisition in history by a meaningful margin, surpassing Exelon's acquisition of Constellation in 2012 and Duke Energy's acquisition of Progress Energy in the same year.

Fig 1: NEE / Dominion - Utility M&A Deal Size Comparison (Source: MKI Global Partners)

Federal Regulatory Approval Overview and Timing

HSR presents minimal risk, as the parties have no overlapping retail service territories. NextEra's Florida franchise and Dominion's Virginia and South Carolina franchises are geographically separated. NEER's unregulated generation footprint creates a theoretical overlap in wholesale markets, but the markets are geographically distinct and competitive in character. A Second Request from the DOJ Antitrust Division is possible but would be unusual; resolution of the initial 30-day waiting period is the base case, with a maximum of 60 days assumed for conservatism, in the event of a pull and refile.

FERC Section 203 carries a statutory 180-day shot clock from the date of a complete application, extendable to a maximum of 360 days total. The practical concern is not timing but the content of the Appendix A competitive analysis. NEER holds substantial generation assets dispatching into PJM, the same wholesale market from which Dominion Energy Virginia purchases power as a load-serving entity. This vertical integration, a competitive generator and a captive load-serving entity under common ownership in the same regional transmission organization (RTO), is exactly the kind of structural concern that FERC's post-2008 merger policy has focused on. FERC Staff will almost certainly require detailed mitigation proposals, potentially including open access commitments, limits on affiliate transactions between NEER and Dominion's load-serving operations, or even structural ring-fencing of NEER's PJM-facing generation assets from the Dominion regulated entities. A complex deficiency letter cycle could consume three to four months of the shot clock, but FERC approval within 12 months from application is a high-confidence base case.

The NRC is the genuine critical path item at the federal level and is probably the single longest elapsed-time approval in the entire stack, ahead even of the Virginia SCC on timing. Dominion operates four nuclear units across two stations: North Anna Units 1 and 2 and Surry Units 1 and 2, all located in Virginia. A change of control application under 10 CFR 50.80 requires NRC Staff review of the technical, financial, and organizational qualifications of the proposed new owner. NextEra already operates nuclear facilities, Turkey Point and St. Lucie in Florida, Seabrook in New Hampshire, and previously Duane Arnold in Iowa, and its NRC track record is strong. However, the NRC process is document-intensive, involves independent safety evaluations for each license, and proceeds on no statutory shot clock whatsoever. The NRC's historical processing time for major license transfer applications in complex transactions runs 12 to 18 months from a complete application. For a four-unit, two-station transfer at two sites with different license structures, 18 months is the prudent working assumption and is likely to be the pacing item relative to FERC on the federal side.

The FCC transfer of control process for utility microwave and point-to-point spectrum licenses is largely administrative and typically resolves within 180 days. It is not a material risk item, but it must be filed and cannot be omitted.

Fig. 2: NEE / Dominion - Regulatory Approval Timeline (Source: MKI Global Partners)

Virginia: The Critical Approval

Under the Virginia Utility Transfers Act, Section 56-90 of the Virginia Code, the SCC must find that the transfer of control will not impair or jeopardize adequate service at just and reasonable rates. Although formally a no-harm standard rather than a mandatory net-benefit test, the SCC has interpreted it with extreme rigor in major proceedings. Given the scale of Dominion's obligations under the VCEA, a mandatory decarbonization schedule written directly into Virginia law, any acquirer must satisfy the commission not merely that service quality will not deteriorate, but that the proposed owner possesses the capital, the technical capacity, and the operational commitment to execute one of the largest utility capital program in the country on a legally binding timeline. That is a much higher practical bar than the statutory language suggests.

The SCC's review would focus on at least four interlocking issues. The first is CVOW operational integration and rate-base prudency risk. With the 2.6 GW Coastal Virginia Offshore Wind project over 70% complete and transitioning out of pure construction risk, the focus will center on long-term operational performance and the final prudency review of the project's expanded $11.5 billion budget. NextEra would need to provide specific capital commitment undertakings, potentially including parent-level guarantees, to satisfy the commission that its capital allocation priorities support this massive offshore asset. The second is ring-fencing and financial insulation, where the SCC would require structural separation ensuring that NEER's competitive generation liabilities, any capital allocation demands from XPLR Infrastructure (NextEra's listed yieldco-style vehicle for contracted renewables and infrastructure assets, operating outside the regulated utility perimeter), and any future NextEra parent-level financial stress could never impair Dominion Energy Virginia's credit rating or grid investment capacity. The third is the VCEA execution timetable. The SCC has been a demanding overseer of Dominion's Integrated Resource Plan (IRP), a plan that outlines the potential ways Dominion can meet future energy demands, while meeting their commitment to reliable, affordable and increasingly clean energy, compliance even as a standalone company. An acquirer must demonstrate that the regulatory timeline embedded in the VCEA will not be traded against NEER's competitive deployment opportunities. The fourth is ratepayer benefits. Virginia consumer advocates will demand concrete, quantifiable consumer benefits - direct rate credits, investment commitments, or rate freezes, tied to the transaction, not vague synergy forecasts. The commission has rejected soft commitments in the past.

The statutory clock under Section 56-88.1 provides the SCC with 60 days from a completed application to rule, extendable by an additional 120 days, for a hard ceiling of 180 days. In practice, the SCC will use the maximum extension and conduct a full evidentiary proceeding. The commission has never faced a transaction of this complexity, and nothing in the statute prevents multiple rounds of supplemental data requests that can toll the practical timeline even if they do not formally toll the shot clock. The true outer limit of a contested Virginia proceeding without rejection could easily exceed 12-18 months from application filing.

The Virginia SCC Commission: Composition and Implications

Kelsey A. Bagot is the current Chair of the commission, a position that rotates annually among the three members. Judge Bagot was elected by the General Assembly in January 2024 to a full six-year term beginning April 1, 2024. She holds a J.D. from Harvard Law School and prior to her election was employed as a Senior Attorney at NextEra Energy, Inc. Before that she served as Legal Advisor to Commissioner Mark C. Christie at FERC, and earlier as a trial attorney at FERC and an associate at Troutman Sanders LLP and Van Ness Feldman LLP. The implication is immediate and serious: Judge Bagot might need to recuse herself from any proceeding arising from a NextEra Energy acquisition of Dominion Energy. Her prior employment relationship with the acquirer creates a direct conflict that standard judicial ethics rules would likely require to be resolved through recusal. How Virginia SCC rules handle such a recusal, whether a retired judge is recalled, whether a two-member panel can lawfully act, and whether a one-to-one deadlock creates an irresolvable impasse, is a central structural uncertainty discussed further in the risks section below. A two-member panel that deadlocks cannot issue a final order, which creates a scenario where the application is neither approved nor denied within the statutory window - a legally unprecedented outcome at the Virginia SCC.

Jehmal T. Hudson is the commission's most experienced member, having served continuously since July 2020 under appointment by Governor Northam and subsequent election to full successive terms by the General Assembly. Judge Hudson holds a B.A. from Adelphi University, a J.D. from Vermont Law School, and an LL.M. in Taxation from Georgetown University Law Center. His prior career was spent at FERC, where he served for approximately ten years in various roles culminating as Director of Government Affairs. He then served as Vice President of Government Affairs at the National Hydropower Association before being elected to the SCC. He serves as the First Vice President of NARUC, chairs the Electric Power Research Institute Advisory Council, and has been the Virginia member of the Organization of PJM States. His background is directly relevant to the issues a NEE/Dominion proceeding would raise: he is deeply familiar with FERC Section 203 standards, PJM market structure, and the intersection of state and federal regulatory jurisdiction.

Samuel T. Towell took office on March 20, 2024, to fill an unexpired term running through January 31, 2028. He holds a B.S. in Mechanical Engineering and Economics from MIT and a J.D. from the University of Virginia School of Law. His career before the SCC was spent in general civil litigation: he was a litigation associate at McGuireWoods LLP and Williams Mullen P.C., served as Virginia's Deputy Attorney General for Civil Litigation, where he supervised the Insurance and Utilities Regulatory Section that appears before the SCC, and then served as Deputy Secretary of Agriculture and Forestry under Democratic Governor Terry McAuliffe and as Special Assistant to the Secretary of Finance under Democratic Governor Mark Warner. His most recent private sector role was Associate General Counsel for Litigation at Smithfield Foods. Judge Towell has no specific energy regulatory background comparable to Judge Hudson's, and his Democratic executive-branch associations and consumer protection background at the AG's office position him to be especially responsive to rate impact and consumer protection arguments.

The practical read on this panel, setting aside the Bagot recusal issue, is a bench that is procedurally rigorous, substantively capable, and not predisposed toward either approval or denial on ideological grounds. What it is not is a rubber stamp. The SCC has denied or heavily conditioned numerous Dominion applications in recent years, including IRP filings, and has shown no reluctance to impose demanding conditions on utilities of any size. The absence of an investor-owned utility-industry insider on the panel means none will be reflexively sympathetic to the capital allocation logic of a large out-of-state acquirer.

South Carolina and North Carolina

North Carolina presents a narrower issue- Dominion Energy North Carolina serves customers in the northeastern part of the state. The North Carolina Utilities Commission (NCUC) operates under a public interest standard that in practice focuses heavily on financial capability and service continuity. The NCUC has historically been procedurally efficient and has approved major utility transactions without the intensity of scrutiny applied by the Virginia SCC. No specific stumbling block is anticipated, but the NCUC would be attentive to VCEA compliance timelines given the NC-VA grid's interconnected nature. Expected timeline is 9 to 12 months from filing.

Some of our conversations suggested that South Carolina may not be a purely mechanical approval, given residual legislative frustration with NextEra following the failed Santee Cooper sale process and broader post-SCANA sensitivity around ratepayer protections. This is unlikely to make South Carolina a deal-breaker, but it could increase pressure on the PSC, ORS and intervenors to extract a more meaningful customer benefit package than would otherwise be required.

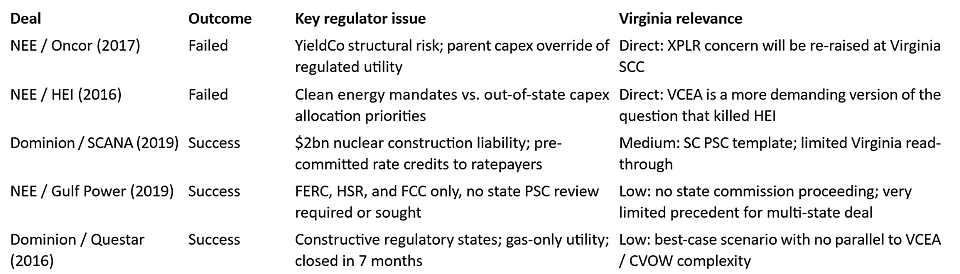

Precedent Transactions: NextEra

NextEra's attempted acquisition of Oncor Electric Delivery is the most relevant cautionary case. Following the Energy Future Holdings bankruptcy, NextEra announced a bid for Oncor in July 2016. The Texas Public Utility Commission held hearings in late 2016 and voted in early 2017 to reject the transaction. The PUCT's central objection was structural: commissioners concluded that NextEra's YieldCo vehicle created a pathway through which Oncor's regulated assets could eventually be exposed to structural risks outside PUCT's direct jurisdictional control without prior approval. The commission also objected to governance provisions that gave the parent excessive control over Oncor's capital expenditure program. NextEra withdrew in March 2017. A similar concern - that XPLR Infrastructure creates a structural pathway for asset integration away from the traditional regulated utility construct - will be raised in every state proceeding for a Dominion acquisition and must be addressed with specific and irrevocable contractual prohibitions at the outset of the application.

NextEra's attempted acquisition of Hawaiian Electric Industries announced in December 2014 failed after the Hawaii Public Utilities Commission issued a decision expressing serious reservations about local employment, management localization, and the interaction between NextEra's capital allocation framework and Hawaii's aggressive clean energy mandates. The parties attempted to address the concerns but ultimately walked away in July 2016 rather than accept conditions that NEE viewed as commercially unacceptable. The Hawaii failure is directly on point for the Virginia VCEA problem: a state commission with aggressive clean energy mandates asked whether an out-of-state acquirer would truly prioritize local renewable build-out against competing capital demands from its broader portfolio. NextEra's answer was insufficiently convincing to move the Hawaii PUC. It will face exactly that question again from the Virginia SCC.

The successful precedents provide a contrasting template: NextEra's $6.5bn acquisition of Gulf Power and Florida City Gas from Southern Company, announced in May 2018 and completed in January 2019, required only FERC section 203, HSR clearance, and FCC approval, no Florida PSC review was required or sought. Because NextEra was acquiring a Florida utility in a non-overlapping service territory from an out-of-state parent, state commission jurisdiction did not attach and the transaction closed in approximately seven months. However, the absence of any contested state commission proceeding means it provided very limited precedent value for a multi-state transaction of the current Dominion scale, which crosses completely independent RTOs.

Precedent Transactions: Dominion

Dominion's acquisition of Questar Corporation, announced February 26, 2016, and closed September 16, 2016, required FERC, HSR, and state commission approvals in Utah, Wyoming, and Idaho. It resolved in approximately seven months. The regulatory straightforwardness reflected Questar's character as a pure natural gas distribution utility in states with generally constructive regulatory environments. The Questar precedent illustrates what a clean regulatory critical path looks like for Dominion, but it has almost no bearing on the complexity of a transaction involving Virginia, the VCEA, and active nuclear assets.

Fig 3: NEE / Dominion - Precedent Transaction Matrix (Source: MKI Global Partners)

The Trump Administration: Federal Policy Environment

The administration's executive orders directing federal agencies to accelerate reviews of energy infrastructure projects have influenced the culture of FERC and DOE reviews, with both agencies adopting somewhat more permissive procedural postures for transactions presenting no horizontal concentration concerns. The DOJ Antitrust Division under the current administration has been markedly less aggressive in utility and infrastructure M&A than its predecessor, making a Second Request in a transaction with no retail overlap highly unlikely. Trump administration appointments to FERC have generally brought a preference for market-oriented regulatory approaches, which marginally reduces the likelihood of FERC requiring draconian structural remedies on the NEER/PJM vertical integration issue, though FERC's Section 203 analysis remains technically independent regardless of political appointments. The administration's support for nuclear energy is relevant to the NRC track. The administration has backed streamlined NRC administrative processes and expressed general support for the continued operation of existing nuclear assets. This creates a somewhat more accommodating NRC environment for the licence transfer at North Anna and Surry, though it does not accelerate the technical safety and financial review timeline meaningfully.

The federal permitting streamlining agenda is largely irrelevant to utility merger review: FERC, NRC, and state commission proceedings are governed by statutes not subject to executive order modification. The Trump administration can neither direct the Virginia SCC nor accelerate the NRC's technical safety review.

There is one indirect channel through which federal policy does matter: Dominion's Coastal Virginia Offshore Wind project depends on a federal lease area granted by the Bureau of Ocean Energy Management and is subject to ongoing federal environmental and construction permits. Given the administration's historical hostility toward offshore wind permitting, any friction introduced into CVOW's ongoing federal regulatory status during the pendency of a merger review could be weaponized by SCC intervenors arguing that an out-of-state acquirer cannot hedge the political and regulatory instability surrounding the asset class.

Risks to Closing

Virginia SCC approval is both the most likely source of delay and the most likely deal-termination mechanism. The combination of VCEA obligations, long-term CVOW performance oversight, the XPLR Infrastructure structural concern resurrected from the Oncor rejection, the Bagot recusal dynamic, and the reconfigured commission's focus on rate impacts creates a risk profile that is significantly wider than any of NEE's prior state commission proceedings. If the SCC denies the application, a refile after Virginia Supreme Court appeal could add three to five years to the timeline. A conditional approval with terms the acquirer finds commercially unacceptable - particularly around capital commitment levels for CVOW, rate freezes of unusual duration, or XPLR ring-fencing provisions that impair NEE's YieldCo capital strategy, could also result in a contested outcome that either party might choose to walk away from. This is not a low-probability scenario.

The Bagot recusal dynamic is analytically separable from the substantive Virginia SCC risk. A two-commissioner panel is constitutionally and procedurally irregular at the Virginia SCC, which was designed as a three-person court of record. Virginia SCC rules provide for recalling retired commissioners to constitute a panel when a vacancy exists, as occurred during the 2021–2024 vacancy period when former Commissioner James Dimitri was recalled repeatedly for 90-day periods. But a recusal scenario arising from a party affiliation mid-proceeding is different from a vacancy and raises distinct procedural questions that have not been extensively litigated at this commission. If a recalled retired judge is substituted, that introduces a further variable into an already complex proceeding, as the retired judge's known regulatory philosophy may differ materially from the current commission's outlook. If no substitute is seated, a 1-1 deadlock between the remaining two commissioners creates an irresolvable procedural impasse that could paralyze the transaction under the statutory timelines of Virginia Code § 56-88.1.

NRC timing risk is real but does not threaten deal completion, only timing. An 18-month NRC track is the base case. A 24-month track is possible if Staff identifies issues with the organizational qualification of the combined entity's nuclear operations, requires revised emergency response arrangements, or imposes conditions requiring renegotiation. NEE's existing nuclear operating record at Turkey Point, St. Lucie, and Seabrook is positive and will be the central credential in the application. The practical mitigation is to file simultaneously with FERC and to begin pre-application engagement with NRC Staff as early as possible.

FERC Section 203 vertical integration risk is the federal approval most likely to produce conditions rather than approval. The mitigation available to the parties, behavioral commitments on affiliate transactions between NEER and Dominion Energy Virginia, a commitment not to transfer Dominion regulated assets to XPLR without prior FERC approval, open access undertakings for NEER's PJM generation output, is well-understood from prior proceedings. FERC has approved complex vertical integration situations with conditions before, including the Exelon/PSEG merger and multiple NextEra precedents. A negotiated condition package, agreed with FERC Staff prior to the formal deficiency letter cycle, would substantially reduce timing risk.

Timeline Summary and Probability Assessment

Accounting for the preparation period required before filing a complete application, typically two to four months following announcement for transactions of this complexity, the realistic range from deal announcement to close spans 20-24 months, pushing the critical path out significantly further than standard consensus estimates. The critical path is determined by whichever of NRC or Virginia SCC takes longer, and those two proceedings, running concurrently, are both capable of extending beyond 18 months.

The probability of completion, on a deal announced, assuming a credible commitment package pre-negotiated with major Virginia intervenors, is moderate. The two failed precedents in NEE's own history, Texas and Hawaii, failed not on antitrust or federal grounds but on the specific question of whether the acquirer could be trusted to subordinate its capital allocation priorities to the state's local regulatory program. The Virginia VCEA is a more demanding and more legally specific version of the same concern that destroyed the Hawaii acquisition. That comparison should give investors considerable pause.

Conclusion

Distribution

This research report and all information contained within is intended for institutional clients of MKI Global Partners and qualified prospective institutional clients and is not meant for redistribution.

Analyst Certification

I, David O’Hara, hereby certify that the views expressed in the foregoing research report accurately reflect my personal views about the subject securities and issuer(s) as of the date of this report. I further certify that no part of my compensation was, is or will be directly, or indirectly, related to the specific recommendations or views contained in this report.

Financial Interests

Neither I, David O’Hara, nor a member of my household has purchased the security (ies) which is/are the subject of this research report. Neither I, nor a member of my household is an officer, director, or advisory board member of the issuer(s) or has another significant affiliation with the issuer(s) that is/are the subject of this research report. I do not know or have reason to know at the time of this publication of any other material conflict of interest.

Important Disclosures

MKI Global Partners is an independent research company and is not a registered investment advisor and is not acting as a broker dealer under any federal or state securities laws.MKI Global Partners is a member of IRC Securities’ Research Prime Services Platform. IRC Securities is a FINRA registered broker-dealer that is focused on supporting the independent research industry. Certain personnel of MKI Global Partners (i.e. Research Analysts) are registered representatives of IRC Securities, a FINRA member firm registered as a broker-dealer with the Securities and Exchange Commission and certain state securities regulators. As registered representatives and independent contractors of IRC Securities, such personnel may receive commissions paid to or shared with IRC Securities for transactions placed by MKI Global Partners clients directly with IRC Securities or with securities firms that may share commissions with IRC Securities in accordance with applicable SEC and FINRA requirements. As registered representatives of IRC Securities, our analysts must follow IRC Securities’ Written Supervisory Procedures. Notable compliance policies include (1) prohibition of insider trading or the facilitation thereof, (2) maintaining client confidentiality, (3) archival of electronic communications, and (4) appropriate use of electronic communications, amongst other compliance related policies.Finally, MKI Global Partners does not have the same conflicts that traditional sell-side research organizations have because MKI Global Partners (1) does not conduct an investment banking activities, (2) does not manage any investment funds, and (3) our clients are only institutional investors.

Company Disclosure

MKI Global Partners has no long or short position in any security of any of the companies mentioned in this report. The Company has no contractual relationship, nor have we received any compensation from any of the companies listed in this research report.