Now that we have a clear winner for Warner Bros. Discovery (WBD US / Market Cap $71bn) in Paramount Skydance (PSKY US / $12bn), we wanted to quickly refresh thoughts on the regulatory backdrop to the combination. The buyer has clearly done a great job already at Federal US level, but there are still various boxes to be ticked. It should also be remembered that deal terms matter alongside the competition issues. Clauses such as regulatory commitments, a $7bn regulatory termination fee, the $0.25 per share per quarter ticking fee beginning after 30 September, and any promise to fight a challenge help frame how the buyer may approach a prolonged review and how far it may be willing to go on remedies if requested. Those terms also affect remedy negotiations because they shape when walking away becomes realistic if regulators demand asset sales that reach core parts of the business.

The immediate antitrust question is not whether streaming is competitive in the abstract. The question is whether regulators define a set of narrower legacy video, advertising, licensing, and production infrastructure markets where overlap is direct, and the competitive story is easier to plead, even if broader subscription video on demand (SVOD) competition remains intense. Most initial commentary will say that streaming is highly competitive, so antitrust should mainly affect timing. That can be true for streaming, but it still misses the real risk. The real risk turns on how regulators define the relevant markets. If they define narrower markets such as premium pay TV networks, cable channel bundles, national TV and CTV advertising, content licensing windows, or Los Angeles sound stage capacity, then the review becomes much tougher, and remedies become the main issue.

A separate process overlay can arise from salience. Heightened federal lobbying around competition in entertainment and streaming can increase third-party engagement and political attention. Any public allegations or scrutiny around bidder financing or foreign sovereign capital, even if not determinative of the competition merits, can create parallel process friction that lengthens timelines and makes behavioural commitments more politically charged to negotiate and monitor.

Antitrust Overview

At a first principles level, this transaction combines two large media and entertainment groups that both supply linear networks, streaming products, national advertising inventory, and content licensing, with additional overlap in elements of production infrastructure. This is predominantly a horizontal combination because the overlap is extensive across multiple sell-side and buy-side contracting points, while genuinely vertical links are narrower and more fact-specific. That matters because horizontal cases give agencies a straightforward path: define the product market, define the geography, then test whether the merger removes a close rival in a way that worsens pricing or non-price outcomes.

The overlap is easiest to understand through how customers buy. Distributors buy bundles of channels and negotiate affiliate fees and carriage terms against a set of rival network owners. Advertisers buy national TV and connected TV (CTV) inventory increasingly as a combined plan, with value tied to scale, data, and the ability to deliver reach across linear and digital. Third-party platforms and broadcasters buy content windows in catalogue libraries and first-run scripted series, where the number of credible sellers can matter as much as raw viewership. Producers and studios buy physical capacity such as sound stages on a local basis, where capacity constraints and scheduling frictions make local overlap especially legible.

Geography is the second lever. Many of the relevant markets are naturally national because contracting is centrally negotiated and distribution is nationwide, including most pay TV carriage, national advertising sales, and content licensing. Two categories are more likely to be analysed locally. Broadcast station-related competition is typically assessed at the designated market area (DMA) level because local stations compete for local ad budgets. Sound stage and studio lot rentals are inherently local because they are tied to physical assets, labour pools, and vendor ecosystems. That is why Los Angeles' production capacity can become a central hook for scrutiny, including from state enforcers.

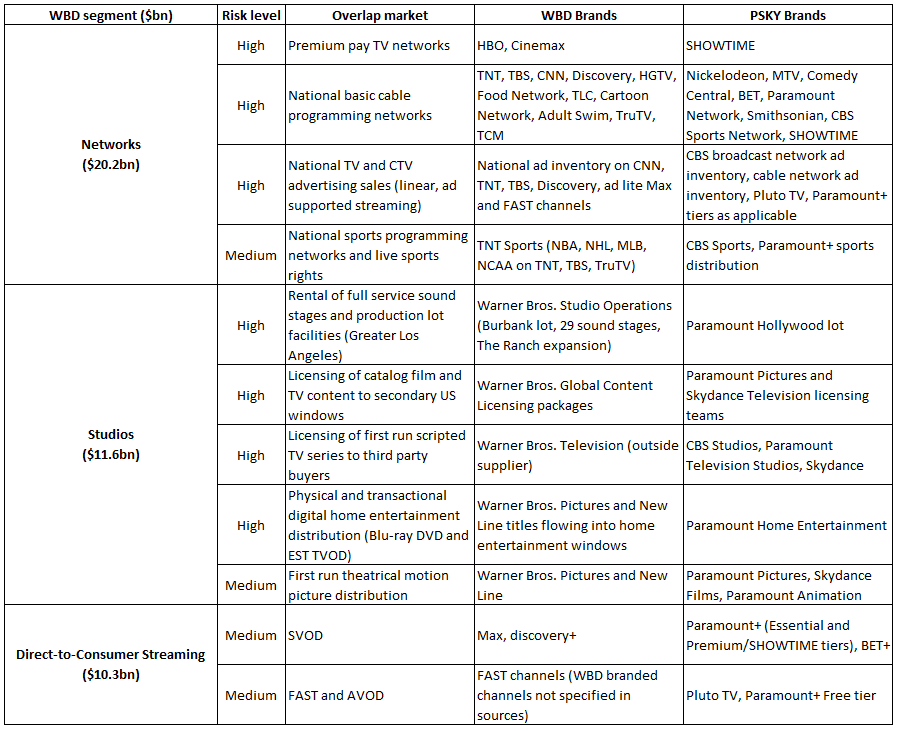

The discussion above explains why the same transaction can look benign under a broad “video” lens but become much harder under narrower, commercially realistic market definitions. To make that distinction concrete, the table below isolates the overlap markets most likely to drive regulatory questions, focusing only on the medium and high risk areas where (i) head to head rivalry is clearest, (ii) geography can be defined tightly where relevant, and (iii) any remedy package, if required, would most plausibly need to be targeted. The purpose of the table is to provide a reader’s map for the likely focus areas in diligence, agency engagement, and remedy planning, without relying on low-confidence market share estimates.

The immediate antitrust question is not whether streaming is competitive in the abstract. The question is whether regulators define a set of narrower legacy video, advertising, licensing, and production infrastructure markets where overlap is direct, and the competitive story is easier to plead, even if broader subscription video on demand (SVOD) competition remains intense. Most initial commentary will say that streaming is highly competitive, so antitrust should mainly affect timing. That can be true for streaming, but it still misses the real risk. The real risk turns on how regulators define the relevant markets. If they define narrower markets such as premium pay TV networks, cable channel bundles, national TV and CTV advertising, content licensing windows, or Los Angeles sound stage capacity, then the review becomes much tougher, and remedies become the main issue.

A separate process overlay can arise from salience. Heightened federal lobbying around competition in entertainment and streaming can increase third-party engagement and political attention. Any public allegations or scrutiny around bidder financing or foreign sovereign capital, even if not determinative of the competition merits, can create parallel process friction that lengthens timelines and makes behavioural commitments more politically charged to negotiate and monitor.

Antitrust Overview

At a first principles level, this transaction combines two large media and entertainment groups that both supply linear networks, streaming products, national advertising inventory, and content licensing, with additional overlap in elements of production infrastructure. This is predominantly a horizontal combination because the overlap is extensive across multiple sell-side and buy-side contracting points, while genuinely vertical links are narrower and more fact-specific. That matters because horizontal cases give agencies a straightforward path: define the product market, define the geography, then test whether the merger removes a close rival in a way that worsens pricing or non-price outcomes.

The overlap is easiest to understand through how customers buy. Distributors buy bundles of channels and negotiate affiliate fees and carriage terms against a set of rival network owners. Advertisers buy national TV and connected TV (CTV) inventory increasingly as a combined plan, with value tied to scale, data, and the ability to deliver reach across linear and digital. Third-party platforms and broadcasters buy content windows in catalogue libraries and first-run scripted series, where the number of credible sellers can matter as much as raw viewership. Producers and studios buy physical capacity such as sound stages on a local basis, where capacity constraints and scheduling frictions make local overlap especially legible.

Geography is the second lever. Many of the relevant markets are naturally national because contracting is centrally negotiated and distribution is nationwide, including most pay TV carriage, national advertising sales, and content licensing. Two categories are more likely to be analysed locally. Broadcast station-related competition is typically assessed at the designated market area (DMA) level because local stations compete for local ad budgets. Sound stage and studio lot rentals are inherently local because they are tied to physical assets, labour pools, and vendor ecosystems. That is why Los Angeles' production capacity can become a central hook for scrutiny, including from state enforcers.

The discussion above explains why the same transaction can look benign under a broad “video” lens but become much harder under narrower, commercially realistic market definitions. To make that distinction concrete, the table below isolates the overlap markets most likely to drive regulatory questions, focusing only on the medium and high risk areas where (i) head to head rivalry is clearest, (ii) geography can be defined tightly where relevant, and (iii) any remedy package, if required, would most plausibly need to be targeted. The purpose of the table is to provide a reader’s map for the likely focus areas in diligence, agency engagement, and remedy planning, without relying on low-confidence market share estimates.

Fig 1: US Focus Overlaps, Grouped by WBD Segment (Source: MKI Research)

United States: DoJ and CA AG

Public reporting indicates that the federal HSR process is past the statutory standstill stage. In a report published last week Bloomberg wrote that Paramount has completed the DoJ’s Second Request process under HSR and that the post compliance waiting period has expired, meaning there is no longer a statutory waiting period that would, by itself, prevent closing in the United States. The same reporting notes the standard caveat that expiry of the waiting period is not an affirmative DOJ approval and does not remove the DOJ’s ability to sue later, but it does shift attention away from federal process mechanics and toward any remaining sources of timing or remedy friction.

On the public record, if there were to be incremental friction, it is most likely to come from California. California Attorney General (AG) Rob Bonta has stated that the California DoJ has an open investigation and has signalled an intention to be vigorous in its review. The most straightforward local lens is Los Angeles production infrastructure, including sound stages and related facilities, which are physical, location-specific, and therefore easier for a state investigation to assess through evidence on access, capacity, pricing, and terms.

California also has flexibility in legal framing because it can pursue claims under state antitrust law and seek injunctive relief in state court. While California courts often look to federal principles for guidance, the state is not required to mirror federal enforcement choices. In parallel, labour market issues can feature more prominently at the state level than in a classic merger screen, particularly if unions and other stakeholders provide a detailed factual record. Policy proposals discussed publicly would make monopsony considerations explicit in a California merger standard. That is not current law, but it signals the direction of travel and increases the likelihood that labour buyer power questions form part of the inquiry.

The balanced US takeaway is that federal statutory process appears to be past the standstill stage, while California has signalled an active review posture. The practical consequence is that the US timing discussion is now less about HSR waiting periods and more about whether California seeks information, commitments, or targeted remedies that could affect the closing path.

Europe: EC and CMA

In Europe, the headline procedural point is that even if the transaction is notified, the EC’s competition assessment is formally EEA-wide, but the evidence collection and effects analysis in media typically “localise” the market by market because many of the relevant competitive dynamics are national in practice. Language feeds, local rights, advertising relationships, and carriage negotiations often differ country by country, so a single Brussels procedure can still become a country-specific substantive screen for wholesale supply of TV channels, TV and video advertising sales, and retail streaming substitution patterns. The practical consequence is that the timetable can be driven by the slowest national evidence base, rather than by the abstract EEA-wide framing.

Poland is the clearest candidate hotspot because WBD owns TVN Group, giving it an unusually strong local broadcasting and advertising footprint relative to many other Member States. Paramount’s Poland presence is concentrated in thematic pay TV channels, particularly kids and entertainment brands such as Nickelodeon and related feeds, plus selected entertainment channels. That combination creates a plausible Poland-specific issue in wholesale supply of thematic channels to pay TV operators, where DG COMP can credibly run a national market test focused on carriage negotiations, bundling leverage, and whether certain kids and family channels are treated as “must-have” inputs for distributors. Poland can also add timing friction outside pure competition merits because media ownership is politically salient and TVN has been treated in public reporting as a strategic asset, creating the possibility of parallel domestic review even if the Commission’s competition case is manageable.

A relevant precedent is Discovery/Scripps (2018), which was notified EEA-wide but substantively driven by Poland. The Commission focused on TVN24 as a potentially “must-have” news channel in Polish pay TV packages and cleared the deal subject to targeted commitments requiring the channel to be offered on a non-exclusive, unbundled basis at a reasonable fee. The lesson is that a single Member State with a strong local asset can shape the intensity of review and the remedy design even where the overall EEA picture appears manageable.

Beyond Poland, the countries most likely to draw DG COMP localised attention are those where a WBD direct-to-consumer rollout and a Sky Showtime presence coincide and where local advertising and pay TV channel negotiation dynamics remain important. Public disclosures around rollout and availability should be treated as inputs for identifying which Member States may see the most evidence requests, even if the Commission’s jurisdiction and remedy perimeter are EEA-wide. The practical consequence is that the Commission can treat the case as EEA-wide for jurisdiction and remedy scope, while still testing the facts in the few Member States where overlaps look most material and where distributors and advertisers are most likely to complain. That is consistent with Commission practice in other complex files, as seen in Kellanova/Mars, and is likely to be the case in transactions such as Kenvue/Kimberly-Clark or Subsea7/Saipem.

Public reporting indicates that the federal HSR process is past the statutory standstill stage. In a report published last week Bloomberg wrote that Paramount has completed the DoJ’s Second Request process under HSR and that the post compliance waiting period has expired, meaning there is no longer a statutory waiting period that would, by itself, prevent closing in the United States. The same reporting notes the standard caveat that expiry of the waiting period is not an affirmative DOJ approval and does not remove the DOJ’s ability to sue later, but it does shift attention away from federal process mechanics and toward any remaining sources of timing or remedy friction.

On the public record, if there were to be incremental friction, it is most likely to come from California. California Attorney General (AG) Rob Bonta has stated that the California DoJ has an open investigation and has signalled an intention to be vigorous in its review. The most straightforward local lens is Los Angeles production infrastructure, including sound stages and related facilities, which are physical, location-specific, and therefore easier for a state investigation to assess through evidence on access, capacity, pricing, and terms.

California also has flexibility in legal framing because it can pursue claims under state antitrust law and seek injunctive relief in state court. While California courts often look to federal principles for guidance, the state is not required to mirror federal enforcement choices. In parallel, labour market issues can feature more prominently at the state level than in a classic merger screen, particularly if unions and other stakeholders provide a detailed factual record. Policy proposals discussed publicly would make monopsony considerations explicit in a California merger standard. That is not current law, but it signals the direction of travel and increases the likelihood that labour buyer power questions form part of the inquiry.

The balanced US takeaway is that federal statutory process appears to be past the standstill stage, while California has signalled an active review posture. The practical consequence is that the US timing discussion is now less about HSR waiting periods and more about whether California seeks information, commitments, or targeted remedies that could affect the closing path.

Europe: EC and CMA

In Europe, the headline procedural point is that even if the transaction is notified, the EC’s competition assessment is formally EEA-wide, but the evidence collection and effects analysis in media typically “localise” the market by market because many of the relevant competitive dynamics are national in practice. Language feeds, local rights, advertising relationships, and carriage negotiations often differ country by country, so a single Brussels procedure can still become a country-specific substantive screen for wholesale supply of TV channels, TV and video advertising sales, and retail streaming substitution patterns. The practical consequence is that the timetable can be driven by the slowest national evidence base, rather than by the abstract EEA-wide framing.

Poland is the clearest candidate hotspot because WBD owns TVN Group, giving it an unusually strong local broadcasting and advertising footprint relative to many other Member States. Paramount’s Poland presence is concentrated in thematic pay TV channels, particularly kids and entertainment brands such as Nickelodeon and related feeds, plus selected entertainment channels. That combination creates a plausible Poland-specific issue in wholesale supply of thematic channels to pay TV operators, where DG COMP can credibly run a national market test focused on carriage negotiations, bundling leverage, and whether certain kids and family channels are treated as “must-have” inputs for distributors. Poland can also add timing friction outside pure competition merits because media ownership is politically salient and TVN has been treated in public reporting as a strategic asset, creating the possibility of parallel domestic review even if the Commission’s competition case is manageable.

A relevant precedent is Discovery/Scripps (2018), which was notified EEA-wide but substantively driven by Poland. The Commission focused on TVN24 as a potentially “must-have” news channel in Polish pay TV packages and cleared the deal subject to targeted commitments requiring the channel to be offered on a non-exclusive, unbundled basis at a reasonable fee. The lesson is that a single Member State with a strong local asset can shape the intensity of review and the remedy design even where the overall EEA picture appears manageable.

Beyond Poland, the countries most likely to draw DG COMP localised attention are those where a WBD direct-to-consumer rollout and a Sky Showtime presence coincide and where local advertising and pay TV channel negotiation dynamics remain important. Public disclosures around rollout and availability should be treated as inputs for identifying which Member States may see the most evidence requests, even if the Commission’s jurisdiction and remedy perimeter are EEA-wide. The practical consequence is that the Commission can treat the case as EEA-wide for jurisdiction and remedy scope, while still testing the facts in the few Member States where overlaps look most material and where distributors and advertisers are most likely to complain. That is consistent with Commission practice in other complex files, as seen in Kellanova/Mars, and is likely to be the case in transactions such as Kenvue/Kimberly-Clark or Subsea7/Saipem.

Paramount has been eager to point out its early engagement with the EC, but pre-notification outreach typically has limited signalling value absent a notifiable transaction and a settled case theory. Paramount’s messaging about having prepared the runway with the EC should therefore be treated as aspirational rather than determinative, particularly where informal engagement occurred before a notifiable deal package was in place. That is not to imply the EC will necessarily be a binding constraint, but rather to note that DG COMP is process-driven and places weight on a complete notification record and market testing rather than informal assurances. Early discussions and stakeholder soundings suggest attention may focus on areas where EU and US dynamics can diverge, including streaming substitution and certain film and content licensing relationships. In that context, Canal+ may be expected to raise concerns, and heightened engagement with French stakeholders would be consistent with that risk. Public reporting has also suggested DG COMP anticipates a procedurally complex file, which can translate into a longer evidence-gathering phase even where ultimate remedies are feasible.

As an aside, recent experience suggests DG COMP has seen prolonged pre-notification phases on several major merger files, and near-term filing volumes may remain uneven. While public comments have indicated that an initial draft of revised Merger Guidelines could be published in April, the timetable and content remain uncertain and are not necessarily aligned across internal stakeholders. Practitioner feedback suggests publication may be closer to late spring, and it remains to be seen whether any guidance refresh materially affects pre-notification duration or the pace of formal filings in the near-term.

Recent conversations in Brussels are often framed around process discipline and continuity, with less visibility on near-term shifts in enforcement priorities. Developments in Washington, including changes in leadership and posture at the DoJ Antitrust Division, may reinforce a preference within DG COMP to avoid abrupt pivots and to position any adjustments as carefully grounded rather than politically driven. The practical implication is an enforcement environment that may prioritise procedural robustness and incrementalism, even as market participants look for clearer signposts on how merger policy will evolve in response to broader economic and industrial conditions.

As an aside, recent experience suggests DG COMP has seen prolonged pre-notification phases on several major merger files, and near-term filing volumes may remain uneven. While public comments have indicated that an initial draft of revised Merger Guidelines could be published in April, the timetable and content remain uncertain and are not necessarily aligned across internal stakeholders. Practitioner feedback suggests publication may be closer to late spring, and it remains to be seen whether any guidance refresh materially affects pre-notification duration or the pace of formal filings in the near-term.

Recent conversations in Brussels are often framed around process discipline and continuity, with less visibility on near-term shifts in enforcement priorities. Developments in Washington, including changes in leadership and posture at the DoJ Antitrust Division, may reinforce a preference within DG COMP to avoid abrupt pivots and to position any adjustments as carefully grounded rather than politically driven. The practical implication is an enforcement environment that may prioritise procedural robustness and incrementalism, even as market participants look for clearer signposts on how merger policy will evolve in response to broader economic and industrial conditions.

In the United Kingdom, the CMA overlay is best treated as a timing and coordination risk rather than the primary merits anchor unless a discrete UK-only market crystallises. The CMA can move quickly to an initial investigation and can impose interim measures that add friction, and UK media deals can attract elevated third-party engagement. That dynamic increases the probability that remedy discussions, if they arise, are negotiated under tighter timetable pressure than in Brussels, particularly if the CMA forms a view early that a clean, separable package is needed to avoid a Phase 2 reference. In the UK, however, media plurality considerations create additional complications.

Conclusion

With the WBD / PSKY spread looking like it is going to trade at about 10% gross, attention will now turn to the deliverability of the transaction and thus the regulatory backdrop. PSKY have painted a bullish picture as part of their negotiation strategy – but there are clearly still hurdles they need to clear. The regulatory focus is likely to be driven less by broad streaming narratives and more by a smaller set of narrower legacy video, advertising, licensing, and production infrastructure markets where market definition and local evidence matter. In the US, the practical focus is on California, given the California Department of Justice’s stated open investigation and the fact that Los Angeles production infrastructure can be assessed on a local, facility-based record. In Europe, the focus would be the EC, with timetable risk largely driven by whether the case localises into a small set of Member States for evidence gathering and market testing. The UK CMA is best viewed as a possible coordination and timing overlay, particularly if it opens a parallel Phase 1 process and considers interim measures.

With the WBD / PSKY spread looking like it is going to trade at about 10% gross, attention will now turn to the deliverability of the transaction and thus the regulatory backdrop. PSKY have painted a bullish picture as part of their negotiation strategy – but there are clearly still hurdles they need to clear. The regulatory focus is likely to be driven less by broad streaming narratives and more by a smaller set of narrower legacy video, advertising, licensing, and production infrastructure markets where market definition and local evidence matter. In the US, the practical focus is on California, given the California Department of Justice’s stated open investigation and the fact that Los Angeles production infrastructure can be assessed on a local, facility-based record. In Europe, the focus would be the EC, with timetable risk largely driven by whether the case localises into a small set of Member States for evidence gathering and market testing. The UK CMA is best viewed as a possible coordination and timing overlay, particularly if it opens a parallel Phase 1 process and considers interim measures.