Fig 1: ZIM Articles of Association (Source: investors.zim.com)

Political sensitivities have been noted due to Hapag-Lloyd’s shareholder base, which includes Qatari and Saudi state-backed investors among its top five shareholders, with two representatives on its supervisory board. Although these holdings do not constitute a controlling stake, it adds a significant geopolitical dynamic to the approval process. The Israeli defence establishment and the Transportation Ministry will continue to actively review the transaction’s implications for national security and for the future of Israel’s strategically important domestic shipping industry, particularly against a backdrop of global overcapacity and rate pressure in the liner market.

FIMI Involvement

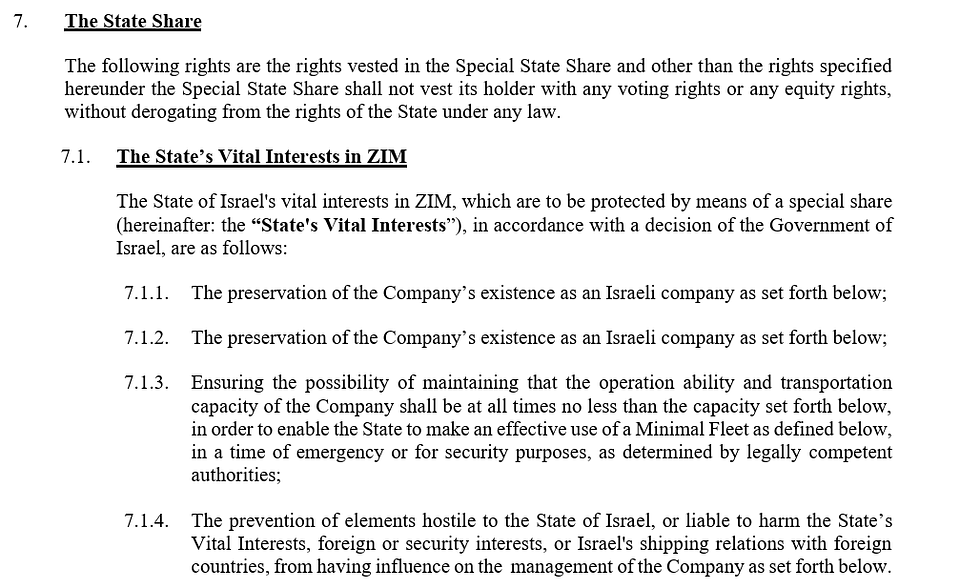

To mitigate political and regulatory risk, the transaction has been structured to preserve Israel’s strategic shipping capabilities. Much of the debate concerns this structure and whether it circumvents the rights under the golden share. A group called FIMI has been baked into the bidding to appease these elements.

FIMI is widely seen as Israel’s leading private equity franchise, with a deep domestic footprint across industrial and infrastructure assets, and a track record of owning and running businesses that sit close to regulated or national-security adjacent end markets. In this transaction FIMI is not window dressing, it is the operating solution that allows the formation and Israeli control of “New ZIM”. Its portfolio spans propulsion and sustainment (Bet Shemesh Engines, jet engine MRO; TAT Technologies, aviation heat transfer), land systems (Ashot Ashkelon, drivetrain components for tanks and APCs, an IDF supplier), and a broad electronics and systems layer (PCB Technologies, Bird Aerosystems, Marom Dolphin, C.Mer Industries). It has also owned assets tied to intelligence and critical infrastructure protection, including ImageSat International and G1 Secure Solutions, plus Orbit Communication Systems which it has since exited. This gives Israeli officials a local counterparty with real credibility on continuity of service, emergency readiness and sensitive supply chains.

FIMI will assume the obligations associated with the golden share by carving out a container liner business serving key strategic lanes to and from Israel, including 16 vessels. This structure satisfies the minimum fleet requirement, retains an Israeli-flagged fleet that could be nationalised in an emergency, and ensures the downsized entity remains headquartered in Haifa. Nevertheless, domestic reports coming out of Israel have flagged concerns that a smaller, FIMI-controlled, carrier might struggle and be a relatively small and underpowered entity in a shipping market exhibiting overcapacity. It is clear that the transaction is a highly politicised topic and has received pushback post-announcement – also seen in Union fronts with ZIM's workers' committee, affiliated with the Histadrut trade union, announcing a 48-hour strike upon the deal's announcement in protest.

We’ve discussed these elements with Hapag-Lloyd this morning, who confirmed to us that much of these negotiations were in the final stages of being completed when the transaction leaked over the weekend, forcing the company to rush out a deal announcement without properly notifying the employees - the company is confident that strikes will cease once employees will hear the benefits of the transaction.

The design of the transaction is clearly calibrated to minimise block risk from the Israeli state. Hapag-Lloyd indicated in its announcement that FIMI’s negotiations with the State regarding consent are “well advanced,” suggesting a pathway to approval, albeit one still subject to political discretion. We have verified with Hapag-Lloyd that preparatory conversations with the Israeli authorities have been a prioritised workstream, with FIMI being the key enabler to navigating national security sensitivities and meeting the golden share conditions. Again it is important to note that the intended announcement sequencing was disturbed by a leak of the transaction which provoked some of the initial employee / union concerns.

Antitrust / Overlap Analysis

This transaction is still a horizontal combination, but not in the “global number one buying number two” sense. Global share is a weak proxy to evaluate antitrust risk in the space and points regulators back to corridor markets (Transpacific, Transatlantic, Asia-Europe), plus service attributes such as direct calls, frequency, and refrigerated capability.

The more interesting competitive questions sit in the “risk pockets” flagged for early diligence: lanes where both parties are meaningful (including certain transpacific niche services and Israel-related trades), the interaction with alliance and slot-exchange structures, and whether Hapag-Lloyd’s terminal and land-side footprint creates any credible foreclosure or information-leverage narrative at particular gateways.

FIMI Involvement

To mitigate political and regulatory risk, the transaction has been structured to preserve Israel’s strategic shipping capabilities. Much of the debate concerns this structure and whether it circumvents the rights under the golden share. A group called FIMI has been baked into the bidding to appease these elements.

FIMI is widely seen as Israel’s leading private equity franchise, with a deep domestic footprint across industrial and infrastructure assets, and a track record of owning and running businesses that sit close to regulated or national-security adjacent end markets. In this transaction FIMI is not window dressing, it is the operating solution that allows the formation and Israeli control of “New ZIM”. Its portfolio spans propulsion and sustainment (Bet Shemesh Engines, jet engine MRO; TAT Technologies, aviation heat transfer), land systems (Ashot Ashkelon, drivetrain components for tanks and APCs, an IDF supplier), and a broad electronics and systems layer (PCB Technologies, Bird Aerosystems, Marom Dolphin, C.Mer Industries). It has also owned assets tied to intelligence and critical infrastructure protection, including ImageSat International and G1 Secure Solutions, plus Orbit Communication Systems which it has since exited. This gives Israeli officials a local counterparty with real credibility on continuity of service, emergency readiness and sensitive supply chains.

FIMI will assume the obligations associated with the golden share by carving out a container liner business serving key strategic lanes to and from Israel, including 16 vessels. This structure satisfies the minimum fleet requirement, retains an Israeli-flagged fleet that could be nationalised in an emergency, and ensures the downsized entity remains headquartered in Haifa. Nevertheless, domestic reports coming out of Israel have flagged concerns that a smaller, FIMI-controlled, carrier might struggle and be a relatively small and underpowered entity in a shipping market exhibiting overcapacity. It is clear that the transaction is a highly politicised topic and has received pushback post-announcement – also seen in Union fronts with ZIM's workers' committee, affiliated with the Histadrut trade union, announcing a 48-hour strike upon the deal's announcement in protest.

We’ve discussed these elements with Hapag-Lloyd this morning, who confirmed to us that much of these negotiations were in the final stages of being completed when the transaction leaked over the weekend, forcing the company to rush out a deal announcement without properly notifying the employees - the company is confident that strikes will cease once employees will hear the benefits of the transaction.

The design of the transaction is clearly calibrated to minimise block risk from the Israeli state. Hapag-Lloyd indicated in its announcement that FIMI’s negotiations with the State regarding consent are “well advanced,” suggesting a pathway to approval, albeit one still subject to political discretion. We have verified with Hapag-Lloyd that preparatory conversations with the Israeli authorities have been a prioritised workstream, with FIMI being the key enabler to navigating national security sensitivities and meeting the golden share conditions. Again it is important to note that the intended announcement sequencing was disturbed by a leak of the transaction which provoked some of the initial employee / union concerns.

Antitrust / Overlap Analysis

This transaction is still a horizontal combination, but not in the “global number one buying number two” sense. Global share is a weak proxy to evaluate antitrust risk in the space and points regulators back to corridor markets (Transpacific, Transatlantic, Asia-Europe), plus service attributes such as direct calls, frequency, and refrigerated capability.

The more interesting competitive questions sit in the “risk pockets” flagged for early diligence: lanes where both parties are meaningful (including certain transpacific niche services and Israel-related trades), the interaction with alliance and slot-exchange structures, and whether Hapag-Lloyd’s terminal and land-side footprint creates any credible foreclosure or information-leverage narrative at particular gateways.

- United States: Operational agreements (alliances/VSAs) can benefit from limited antitrust immunity when filed with the Federal Maritime Commission (FMC), and the Hapag-Lloyd/Maersk Gemini cooperation is cited as an example of an FMC-filed arrangement that attracted attention and oversight. A deal of this nature, however, remains subject to general US merger control, including HSR, and potential DOJ/FTC review.

- Regulators will look into how the two carriers deploy capacity and how their cooperation agreements work. Even so, the competitive read-through should stay corridor-by-corridor, not based on global share. The main concerns are i) the deal could remove direct head-to-head rivalry on specific trade lanes, ii) in a concentrated industry where carriers already work closely through alliances and VSAs, combining the businesses could put more information in one place, which can make it easier for the market to keep capacity tight and for surcharges to move in step. Nonetheless, due to the limited overlap in operations, this doesn't seem like a deal that will raise many concerns from an antitrust perspective.

- European Union: If EU Merger Regulation thresholds are met, the European Commission would be the lead reviewer, otherwise national authorities may be in play. It's worth noting that the EU backdrop is also less forgiving than in prior cycles given the expiry of the Consortia Block Exemption Regulation (CBER) in April 2024, a framework that exempted liner shipping consortia from antitrust rules and allowed shipping lines to cooperate (operate the same routes and slots, share vessels, etc. provided that the shippers had a market share of <30%). In 2024, the EC has found that CBER wasn't effective in facilitating cooperation, especially among smaller operators which therefore didn't have an easier time competing with larger competitors.

- The EC's review will be focused on corridor-by-corridor overlap mapping, and, if needed, it might require route-specific commitments (service transfers, slots, capacity releases), plus potential governance ring-fencing for Israel-related operations. Due to the limited overlap, that reads more as a Phase I type of process than anything else.

Conclusion

The key to this transaction isn’t antitrust (which looks manageable, market share and monopoly concerns are highly unlikely to be the make-or-break). The real gating item is Israel, and the debate is already very much in that direction. Local scrutiny and pushback on the press is not just about whether “New ZIM” owned by FIMI satisfy the Israeli government, it is about whether Israel is effectively giving up control over international lift at a moment when resilience matters most, and whether a downsized Israel-facing carrier would have the scale and balance sheet to perform in a national emergency. Hapag-Lloyd’s register doesn't help the optics - the Saudi and Qatari state-backed entities owning ~22% of the German shipper raise questions as to whether Hapag-Lloyd would place Israel's interests ahead of profits should the need arise. What we have been told this morning backs up that which common sense suggests, that there have been discussions with the Israeli government prior to the deal announcement. FIMI is the key piece of the puzzle, they are serious players locally. FIMI will hence assume the golden share obligations around Israeli ownership and management, minimum fleet capacity and emergency-readiness. That positioning also makes FIMI the natural interlocutor with the relevant ministries, and gives the Israeli government a domestic counterparty with both incentives and experience, rather than relying on undertakings from a German acquirer.

The design of the transaction is clearly calibrated to minimise block risk from the Israeli state. Hapag-Lloyd indicated in its announcement that FIMI’s negotiations with the State regarding consent are “well advanced,” suggesting a pathway to approval, albeit one still subject to political discretion. We have verified with Hapag-Lloyd that preparatory conversations with the Israeli authorities have been a prioritised workstream, with FIMI being the key enabler to navigating national security sensitivities and meeting the golden share conditions. Again it is important to note that the intended announcement sequencing was disturbed by a leak of the transaction which provoked some of the initial employee / union concerns.

Common sense suggests it is highly unlikely we would get a transaction of this nature being announced without sufficient support from the Israeli government but local press has given people pause for thought on this topic this morning – and it is for this reason the spread is going to trade with a >15% spread to the implied price. Until that approval is in the rear view mirror, such a spread is likely to prevail.

The key to this transaction isn’t antitrust (which looks manageable, market share and monopoly concerns are highly unlikely to be the make-or-break). The real gating item is Israel, and the debate is already very much in that direction. Local scrutiny and pushback on the press is not just about whether “New ZIM” owned by FIMI satisfy the Israeli government, it is about whether Israel is effectively giving up control over international lift at a moment when resilience matters most, and whether a downsized Israel-facing carrier would have the scale and balance sheet to perform in a national emergency. Hapag-Lloyd’s register doesn't help the optics - the Saudi and Qatari state-backed entities owning ~22% of the German shipper raise questions as to whether Hapag-Lloyd would place Israel's interests ahead of profits should the need arise. What we have been told this morning backs up that which common sense suggests, that there have been discussions with the Israeli government prior to the deal announcement. FIMI is the key piece of the puzzle, they are serious players locally. FIMI will hence assume the golden share obligations around Israeli ownership and management, minimum fleet capacity and emergency-readiness. That positioning also makes FIMI the natural interlocutor with the relevant ministries, and gives the Israeli government a domestic counterparty with both incentives and experience, rather than relying on undertakings from a German acquirer.

The design of the transaction is clearly calibrated to minimise block risk from the Israeli state. Hapag-Lloyd indicated in its announcement that FIMI’s negotiations with the State regarding consent are “well advanced,” suggesting a pathway to approval, albeit one still subject to political discretion. We have verified with Hapag-Lloyd that preparatory conversations with the Israeli authorities have been a prioritised workstream, with FIMI being the key enabler to navigating national security sensitivities and meeting the golden share conditions. Again it is important to note that the intended announcement sequencing was disturbed by a leak of the transaction which provoked some of the initial employee / union concerns.

Common sense suggests it is highly unlikely we would get a transaction of this nature being announced without sufficient support from the Israeli government but local press has given people pause for thought on this topic this morning – and it is for this reason the spread is going to trade with a >15% spread to the implied price. Until that approval is in the rear view mirror, such a spread is likely to prevail.